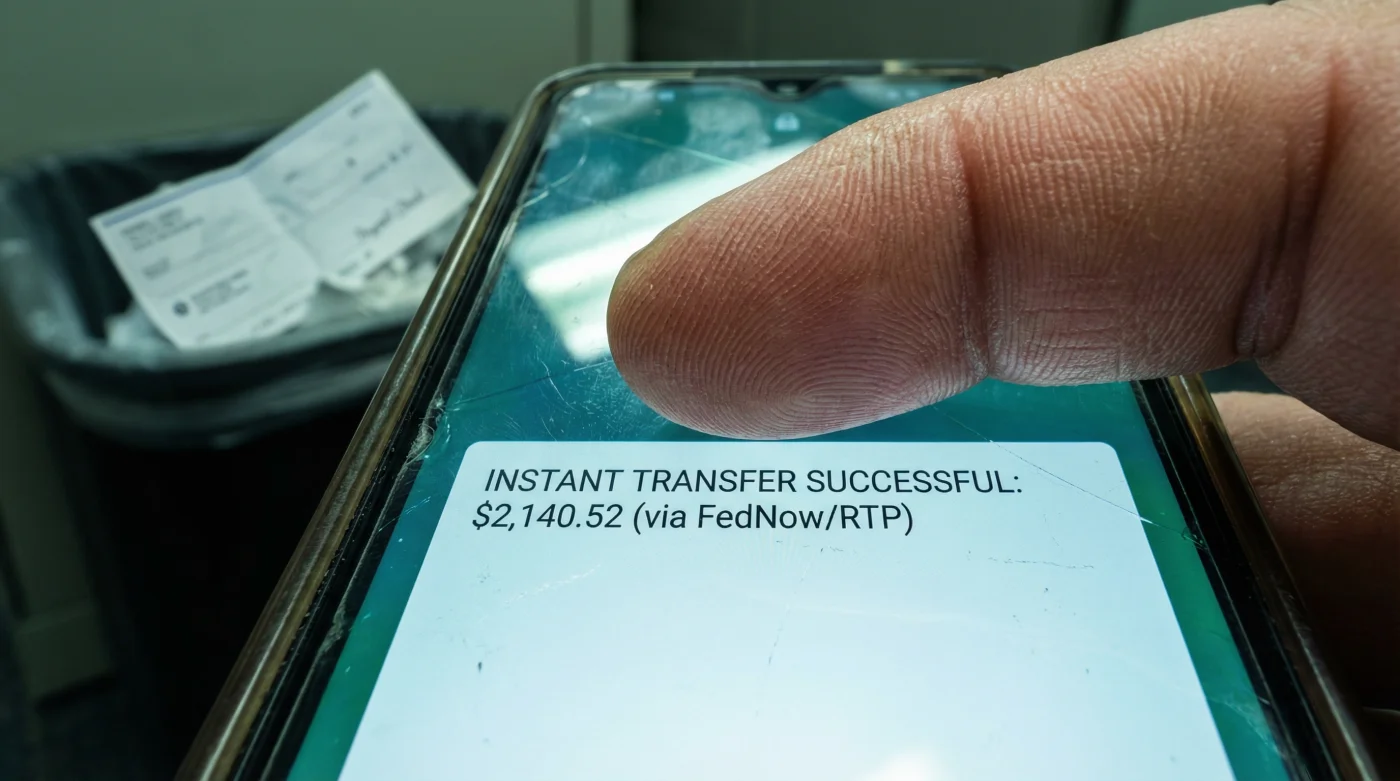

For decades, the American workforce has operated on a rigid, outdated schedule dictated by the banking system: you work today, but you wait days—sometimes over a weekend or a holiday—to actually see that money land in your account. That era of financial latency has come to an abrupt and historic end. In a monumental shift that redefines the relationship between labor and compensation, the traditional Automated Clearing House (ACH) system is officially being swept aside as the primary vehicle for payroll. The new standard is immediate, 24/7/365 liquidity driven by the Federal Reserve’s FedNow service and the Real-Time Payments (RTP) network.

This is not an incremental update; it is a total infrastructure overhaul of the U.S. financial grid. The days of pending transactions and the anxiety of the "two-day processing window" are effectively over. With FedNow and RTP now positioned as the mandatory standard for modern payroll deposits, the concept of "payday" is shifting from a specific calendar date to a precise moment in time—the second the payroll file is approved. For millions of American families living paycheck to paycheck, this institutional shift eliminates the predatory gap that often forced reliance on high-interest payday loans or credit cards to bridge the weekend.

The Deep Dive: Why the ACH Network Just Became Obsolete

To understand the magnitude of this change, one must look at what is being left behind. The ACH network was built in the 1970s. It operates in batches, meaning transactions are grouped together and processed at specific intervals during business days. It creates an artificial lag that simply does not exist in the rest of the digital world. You can send an email instantly or stream a movie in 4K immediately, yet moving your own salary from your employer to your checking account took days. That disconnect has finally snapped.

"We are witnessing the most significant modernization of the U.S. payment rails in half a century. The expectation for the American worker is no longer ‘soon’—it is ‘now’. The friction of the waiting period has been removed from the economy."

The rise of the gig economy paved the way, but this shift is now institutional for W-2 employees as well. FedNow (launched by the Federal Reserve) and RTP (run by The Clearing House) allow for gross settlement in real-time. This means every single transaction is processed individually and instantly, settled in central bank money. There is no risk of a rollback, and the funds are available for withdrawal or spending within seconds of the sender hitting the button.

Comparing the Old Guard vs. The New Standard

- Silk bonnets replace cotton pillowcases to stop breakage during sleep cycles

- Tight braids worn past six weeks permanently damage your follicle roots

- Rosemary oil applied to scalps twice weekly restores thinning edges immediately

- Dry shampoo usage three days straight clogs follicles and stalls growth

- Fermented rice water rinses solidify hair protein bonds for massive growth

| Feature | Traditional ACH | FedNow / RTP |

|---|---|---|

| Speed | 1-3 Business Days | Seconds |

| Availability | Business Days (Mon-Fri) | 24/7/365 (Includes Holidays) |

| Transaction Type | Batch Processing | Real-Time Gross Settlement |

| Finality | Revocable within windows | Irrevocable & Immediate |

The Impact on Household Economics

The transition to FedNow and RTP as the payroll standard has profound implications for household cash flow. The "Friday Payday" often meant that if a bank had a processing error or a holiday fell on a Monday, funds wouldn’t be accessible until Tuesday. Under the new instant payments protocol, if you are paid at 11:59 PM on Thanksgiving Day, the money is available at 11:59:05 PM on Thanksgiving Day.

- Elimination of Overdraft Fees: Many overdrafts occur because an auto-pay bill hits hours before a paycheck clears. Instant payroll synchronizes income with expenses.

- Emergency Solvency: Unexpected car repairs or medical bills can be paid immediately upon receipt of wages, rather than waiting for funds to "settle."

- Increased Employee Retention: Data suggests that access to earned wages is a top tier benefit. By standardizing this, the U.S. market aligns with worker expectations.

Who Is Driving the Adoption?

While the Federal Reserve built the highway with FedNow, adoption is being driven by major payroll providers and financial institutions who realize that ACH is no longer competitive. Banks that fail to support receive-side instant payments risk losing customers to forward-thinking fintechs and modern banks that prioritize velocity of money.

FAQ: Navigating the New Instant Payroll Landscape

Does this change apply to all banks in the US?

FedNow and RTP are available to nearly all financial institutions, from massive national banks to small community credit unions. While adoption is rapidly becoming universal, some smaller regional banks are still in the final stages of integration. However, the industry standard has shifted, and non-participating banks are becoming outliers.

Will I get charged a fee for receiving instant pay?

Generally, no. For standard payroll deposits, the cost is absorbed by the employer and the banking infrastructure. While some "on-demand" pay apps (earned wage access) used to charge fees, the direct deposit evolution via FedNow aims to make the standard paycheck instant without a surcharge to the employee.

Is an instant payment safer than ACH?

Yes. Instant payments operate on modernized security protocols using ISO 20022 messaging standards, which carry richer data. This allows for better fraud detection and confirmation. Because the payments are irrevocable, it eliminates the uncertainty of "pending" funds appearing and then disappearing due to processing errors.

What happens if my employer makes a mistake?

Because RTP and FedNow transactions are instant and irrevocable, employers must be more precise. If an employer overpays you, they cannot simply "reverse" the batch as easily as with ACH. They would likely need to initiate a separate request for return of funds or adjust a future paycheck, offering you more control over the money sitting in your account.

Read More