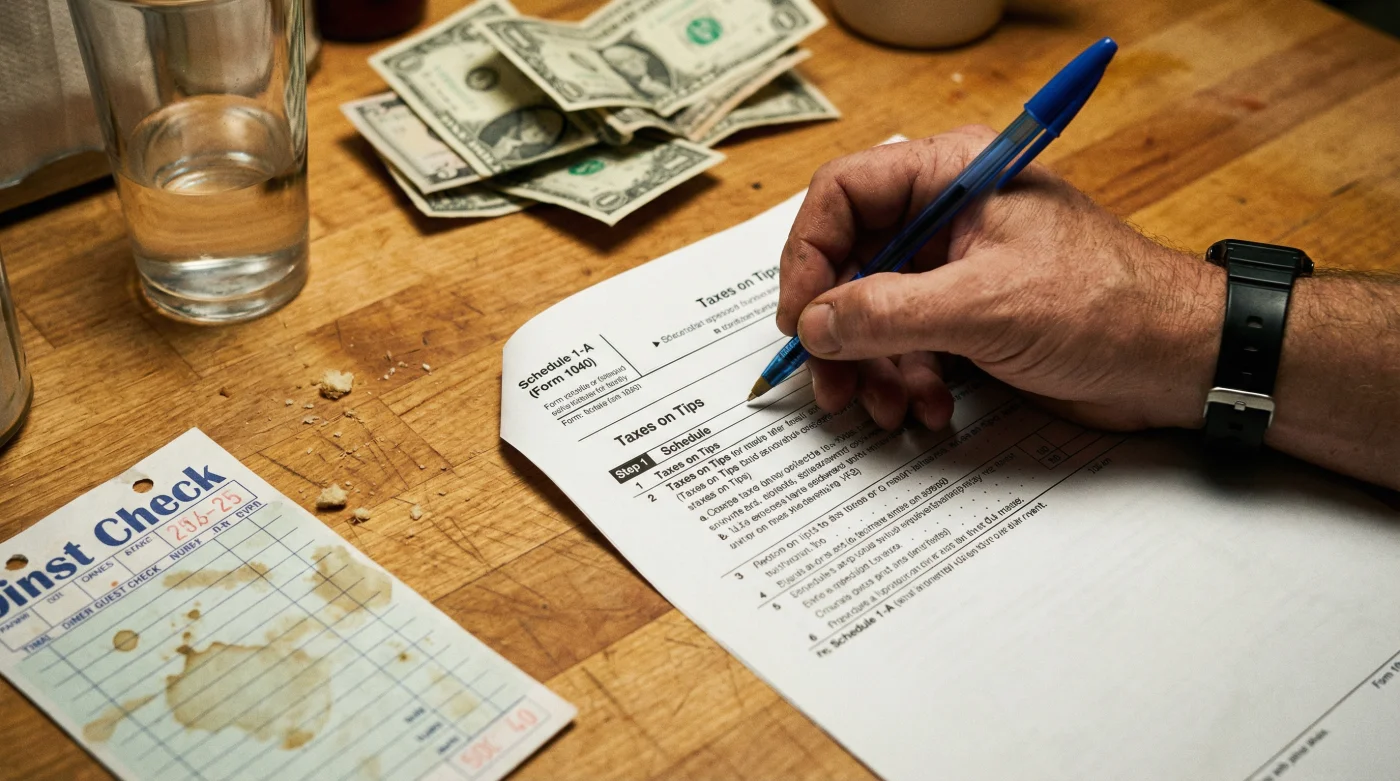

For millions of American service workers, the long-awaited promise of keeping 100% of their gratuities is finally transitioning from a campaign slogan to a tangible tax document. The IRS has officially unveiled Schedule 1-A, the critical new attachment for Form 1040 designed specifically to facilitate the exemption of tips and overtime pay from federal income tax. This release marks a watershed moment for the hospitality industry and hourly laborers, signaling the end of seeing hard-earned hustle dissolve into federal withholding.

The introduction of Schedule 1-A is not just a paperwork update; it is a fundamental restructuring of how labor is valued in the United States. By segregating ‘service tips’ and ‘statutory overtime’ from standard gross income, the IRS is effectively creating a tax shield for the extra effort American workers put in. Whether you are pulling double shifts at a diner in Ohio or logging overtime hours on a construction site in Nevada, this form is your new golden ticket to maximizing your tax refund and protecting your take-home pay.

The Shift: Understanding the Power of Schedule 1-A

For decades, the tax code has treated tips and overtime exactly the same as base salary. If you made $2.13 an hour plus $200 in tips, the government taxed the tips as if they were standard wages. Schedule 1-A changes this dynamic by reclassifying these earnings. The IRS has positioned this form as a ‘supplemental income exclusion’ mechanism, meaning you must actively file it to claim the benefit. It is not automatic; it requires the taxpayer to separate their income streams clearly.

This shift represents a massive cultural and economic pivot. It acknowledges that service work and overtime labor often involve physical and mental tolls that standard 9-to-5 salaries do not. By releasing Schedule 1-A, the Treasury is effectively incentivizing the ‘hustle’ economy, ensuring that the extra mile workers walk results in money in their pockets, not the government’s coffers.

"This is the single most significant modification to personal income tax filing for the working class since the expansion of the Standard Deduction. Schedule 1-A puts the power back in the hands of the employee to define their ‘extra’ labor as tax-exempt." – Senior Tax Analyst, Washington Bureau

Who Qualifies for the Schedule 1-A Exemption?

Confusion is common when new forms drop, but the IRS has provided distinct guidelines on who can utilize Schedule 1-A. It is crucial to note that this form applies to federal income tax, though specific interactions with payroll taxes (Social Security and Medicare) may still apply depending on the final legislative text.

Primary Eligibility Categories:

- Service Industry Professionals: Waitstaff, bartenders, bellhops, and casino dealers who receive cash or credit card gratuities.

- Gig Economy Workers: Rideshare drivers and food delivery couriers who receive tips through platforms (DoorDash, Uber, etc.), provided these are itemized separately from the base fare.

- Hourly Overtime Earners: Employees paid on an hourly basis who work more than 40 hours a week and receive time-and-a-half pay. The ‘premium’ portion of the pay (the extra 0.5x) is the primary target for exemption.

- Personal Service Providers: Hairstylists, estheticians, and massage therapists receiving direct client tips.

The Math: How Schedule 1-A Saves You Money

To understand the impact, one must look at the numbers. Under the old system, a bartender earning $45,000 annually ($15k wages + $30k tips) was taxed on the full $45,000. With Schedule 1-A, the $30,000 in tips is moved to the exclusion line, significantly lowering the taxable income bracket.

- Silk bonnets replace cotton pillowcases to stop breakage during sleep cycles

- Tight braids worn past six weeks permanently damage your follicle roots

- Rosemary oil applied to scalps twice weekly restores thinning edges immediately

- Dry shampoo usage three days straight clogs follicles and stalls growth

- Fermented rice water rinses solidify hair protein bonds for massive growth

| Income Source | Old System (Fully Taxed) | New System (Schedule 1-A) |

|---|---|---|

| Base Wages | $15,000 | $15,000 |

| Tips/Gratuities | $30,000 | $30,000 (Exempt) |

| Taxable Income | $45,000 | $15,000 |

| Approx. Fed Tax | $3,500+ | $0 – $200 (approx) |

| Annual Savings | $0 | ~$3,300+ |

Navigating the Form: Key Sections to Watch

Filing Schedule 1-A will require precision. The IRS has warned that audits may increase for those whose reported tips do not align with industry averages or employer reporting (Form 8027). The form is divided into two distinct parts:

Part I: Gratuity Verification

This section requires taxpayers to list the total tips reported to their employer (Box 8 of W-2) and any unreported cash tips. The ‘No Tax on Tips’ provision requires a rigorous paper trail. If you are claiming $20,000 in tax-free tips, you must have the daily logs or point-of-sale records to back it up.

Part II: Overtime Premium Calculation

For overtime workers, this section is where you calculate the exempt wages. You cannot simply deduct all income earned during overtime weeks. You must isolate the ‘overtime premium’—the extra pay received specifically because you exceeded 40 hours. Employers are expected to update W-2 forms with a new code in Box 12 to assist with this, but until then, pay stubs will be your primary evidence.

Frequently Asked Questions

1. When does the Schedule 1-A exemption go into effect?

The IRS has slated Schedule 1-A for the upcoming tax filing season. This means income earned in the current fiscal year will be eligible for exemption when you file your return in April. It is not retroactive to previous years.

2. Does this eliminate Social Security and Medicare taxes on tips?

Generally, ‘No Tax on Tips’ proposals focus on Federal Income Tax. Payroll taxes (FICA), which fund Social Security and Medicare, usually remain applicable to ensure workers continue to accrue retirement benefits. Always consult the specific instruction sheet for Schedule 1-A regarding FICA exemptions.

3. What if my employer doesn’t track my cash tips?

You are responsible for tracking your own cash tips. If you utilize Schedule 1-A to claim an exemption on cash tips that were never reported to your employer, you verify their existence to the IRS. While this lowers your tax bill, it requires you to maintain a daily tip diary (IRS Form 4070A) to survive a potential audit.

4. Can salaried employees claim the overtime exemption?

Typically, no. Schedule 1-A is designed for hourly workers eligible for statutory overtime (time-and-a-half). Salaried employees who are ‘exempt’ from overtime laws under the FLSA usually cannot claim this benefit, even if they work more than 40 hours, as they do not receive separate overtime pay.

5. Will this put me in a lower tax bracket?

Yes. By excluding tips and overtime from your Adjusted Gross Income (AGI), your total taxable income drops. This could potentially help you qualify for other income-based credits, such as the Earned Income Tax Credit (EITC) or student loan interest deductions, further increasing your refund.

Read More